{kind=link}

Managing receivables doesn’t usually break all at once. It starts with small gaps, missed follow-ups, unresolved disputes, or forecasts based on outdated assumptions.

Over time, those gaps turn into slower collections and less predictable cash flow. That’s where the best credit and collections software becomes essential.

If you’re evaluating tools, it’s likely because something in your current process isn’t scaling. Maybe collections are taking longer, visibility into receivables is limited, or credit decisions feel inconsistent.

To find out what actually works, I analyzed verified G2 reviews and real-world feedback from finance teams across mid-market companies, enterprise shared services, and fast-growing SaaS businesses. I also looked at where tools fall short, because the wrong platform can slow collections, weaken credit controls, and quietly increase risk over time.

In this guide, I’ve shortlisted the best credit and collections software and mapped them to common finance challenges, so you can choose the right platform for your workflows.

10 best credit and collections software for 2026: My top picks

- Billtrust: Best for complex B2B invoice-to-cash workflows

Chosen by finance teams that need structured invoice delivery, digital payments, and collections workflows at scale, across customers. - Creditsafe: Best for credit risk assessment and business credit monitoring

Often used when credit teams need reliable company data, risk signals, and monitoring to inform credit decisions upfront. - HighRadius Accounts Receivables: Best for enterprise AR automation

Commonly used by large finance teams that rely on AI-driven prioritization, forecasting, and collections automation across high invoice volumes. - Quadient AR Automation by YayPay: Best for automated payment follow-ups

Chosen by teams that want automated outreach, promise tracking, and prioritization without heavy process overhead. - Tesorio: Best for treasury visibility and cash forecasting tied to collections signals

Often picked when finance leaders want clearer cash projections connected directly to AR performance and customer payment behavior. - Upflow: Best for modern collections workflows with customer-friendly follow-up

Commonly picked by scaling finance teams that want structured collections processes without rigid enterprise tooling. - Gaviti: Best for AR automation with configurable collections policies

Useful when teams need flexible rules, customer segmentation, and workflow customization without deep technical setup. - Global Database Risk Intelligence: Best for global company risk intelligence

Chosen when credit decisions depend on global business data, risk indicators, and cross-border visibility. - Versapay: Best for collaborative AR and buyer-facing payment experiences

Strong option when teams want shared visibility across sellers and buyers, with built-in collaboration around invoices and disputes. - Resolve: Best for AI-assisted collections and dispute resolution workflows

Commonly picked by teams that want automation support for outreach, dispute handling, and prioritization without losing human control over customer interactions.

*These credit and collections tools are top-rated according to G2’s Winter Grid Report. I’ve highlighted their primary strengths. Pricing information is available on request.

10 best credit and collections software I recommend

Credit and collections software consolidates the mechanics of receivables into a single operational layer. It brings credit assessment, collections prioritization, dispute tracking, and customer communication into one place, instead of leaving them scattered across spreadsheets, inboxes, and ERP exports.

The strongest tools help teams understand why payments stall, which customers need attention first, and what action should happen next. Whether that means surfacing dispute activity, prioritizing accounts based on risk and value, or automating follow-ups without losing visibility into exceptions.

What stands out across G2 reviews is how quickly manual processes start to break once invoice volume increases. Teams adopt these tools not because they want more features, but because they need consistency; clear ownership, predictable follow-ups, and fewer gaps between systems.

At that point, the value becomes straightforward. You get a clearer view of cash risk, more predictable collections performance, and fewer surprises tied to missed invoices or unresolved disputes.

How did I find and evaluate the best credit and collections software?

The shortlist began with G2’s Winter 2026 Grid Report for the credit and collections category, where I filtered platforms by verified user satisfaction scores and market presence across small businesses, mid-market teams, and enterprises.

From there, AI-driven analysis across hundreds of verified G2 reviews helped surface what actually matters in live finance workflows including feature checklists and recurring signals about how teams use these tools under real conditions. That included credit risk assessment, collections prioritization, dispute handling, promise tracking, automation depth, ERP and accounting integrations, and visibility into cash flow and aging.

I haven’t personally used every platform covered here. Findings are validated against publicly shared feedback from accounting, credit, and collections practitioners who actively rely on these tools. All visuals and product references are sourced from G2 vendor listings and publicly available product documentation.

What makes the best credit and collections software worth it: My criteria

To find the best credit and collections software, I looked for consistent patterns in G2 reviews and focused on what actually matters in day-to-day finance and collections workflows.

- Collections prioritization: Tools that flood teams with aging tables, undifferentiated alerts, or generic task lists slow decisions and spread effort thin. The best platforms surface which accounts, invoices, or disputes need attention now, grounded in risk, balance size, and urgency. Without that signal clarity, collectors work harder on the wrong things.

- Workflow alignment: Strong platforms reflect how invoices actually move from issue to payment, including credit checks, partial payments, disputes, promises, and exceptions. Systems that assume linear workflows tend to break under real conditions. When the tool doesn’t match reality, teams work around it and lose control.

- Dispute visibility: Disputes are a core part of collections, not an edge case. G2 reviews consistently flag breakdowns when disputes are managed outside the system. The best tools keep them tracked, visible, and tied to the right invoices and customers, preventing silent stalls that distort cash forecasts.

- Automation with preserved oversight: Automation only helps when it removes repetitive work without creating blind spots. Strong tools automate follow-ups, reminders, and task creation while keeping humans in control of exceptions. Weak automation generates noise or false confidence about account status.

- Cash forecasting connectivity: Collections should strengthen forecast confidence, not operate in isolation from it. Platforms that don’t connect collections signals to cash visibility force finance teams to reconcile data manually and explain variance after the fact. Strong integration between AR activity and forecasting reduces surprises and builds trust in the numbers leadership is seeing.

Based on these criteria, I narrowed down the platforms that consistently help teams reduce uncertainty, recover cash more predictably, and maintain confidence in their collections operations. The right choice depends on whether your priority is risk control, recovery speed, forecasting confidence, or operational efficiency.

Below, you’ll find authentic G2 user reviews from the Credit and Collection Software category. To appear in this category, a tool must:

- Support structured credit management, collections, or dispute workflows

- Be used by accounting, credit, or collections teams as part of ongoing operations

- Integrate with accounting, ERP, or payment systems

- Provide visibility into receivables, risk, and collections activity

The data pulled from G2 is from 2024-2026. Some reviews may not be recent and may have been edited for clarity.

1. Billtrust: Best for complex B2B invoice-to-cash workflows

Billtrust is clearly built to reduce manual AR work as payment volumes and remittance complexity increase. It fits teams operating at scale, where varied remittance formats and ERP-heavy workflows start to slow collections and cash application.

Billtrust automates payment research and remittance matching through OCR and rules-based logic, extracting invoice details from incomplete or messy remits and applying them accurately to open AR items. What I noticed across G2 reviews is that this consistency translates directly into faster payment posting, fewer exceptions, and a high rate of first-pass success, reflected in a collections effectiveness rating of 88% on G2. This shortens close cycles and improves working capital visibility.

The customer portal and financial document capabilities reinforce that reliability on the customer-facing side. G2 reviews rate the customer portal at 91%, pointing to how well the platform supports invoice visibility and document consistency without adding manual effort for internal teams. Review patterns consistently highlight how it makes it easier for customers to view invoices, track payments, and provide remittance details themselves.

From what I saw across G2 reviews, teams dealing with cheque payments consistently point to Billtrust’s reconciliation workflows as a major operational advantage. For organizations processing payments across multiple customer accounts simultaneously, that reduction compounds. Fewer manual touchpoints per transaction means the efficiency gain scales with volume rather than flattening out as workload increases.

What stood out to me across G2 reviews is how often automated invoice and statement distribution came up as a meaningful time-saver. Teams describe moving away from manual batching, with scheduled delivery and bulk statement sends now handled automatically, and match invoices and payments scores 87% on G2. In high-volume environments, that shift frees AR staff for higher-value work and removes a predictable delay in payment initiation.

The onboarding and setup process is easy, the platform becoming familiar quickly even for new users. G2 reviewers specifically call out how Billtrust has simplified credit application handling, replacing paper-based or manual processes with a centralized digital workflow. This ease of entry into core credit and collections functions supports faster deployment and more consistent adoption across AR teams at scale.

Billtrust surfaces real-time delivery confirmation on invoices, showing AR teams exactly when a document was sent, opened, and viewed by the customer. That visibility removes the ambiguity from follow-up conversations. Collectors can confirm receipt rather than accept claims that invoices never arrived. In high-volume environments, having a clear audit trail per invoice keeps dispute handling grounded in fact and shortens resolution cycles.

While overall feedback is strong, G2 reviewers note that teams coming from more visually guided interfaces may find the layout more utilitarian in comparison. This is most noticeable for users prioritizing highly visual navigation, while teams focused on structured AR workflows align well with the platform’s process-oriented design and operational clarity. The interface structure supports consistent navigation and dependable audit visibility across day-to-day receivables operations.

Exception handling follows a defined remittance logic built around standardized payment flows. Teams that regularly process transactions with incomplete or non-standard remittance details will notice this boundary more than others. The structured exception framework aligns well with predictable resolution workflows and controlled review processes across high-volume environments. This approach supports accurate reconciliation and consistent handling of payment exceptions at scale.

Billtrust is well suited for mature credit and collections teams that want to reduce manual effort without losing control or visibility. Its strengths in customer self-service and remittance-driven accuracy stand out in day-to-day AR workflows, which helps explain why it remains a strong choice in complex invoice-to-cash environments.

What I like about Billtrust:

- Automates payment matching and cash application, reducing ERP effort and improving first-pass accuracy.

- Customer-facing invoice and payment portals reduce back-and-forth and support more predictable collections at scale.

What G2 users like about Billtrust:

“Billtrust makes it easy to research payments, account ID, correlation assist makes the work easy and fast to match with the remit, G2’s best AR automation software.”

– Billtrust review, Harish K.

What I dislike about Billtrust:

- The interface prioritizes auditability and process control, which means teams coming from lighter tools may need a short settling-in period before daily navigation feels fully natural. It also reinforces standardized operations across teams, helping maintain alignment in compliance-driven processes.

- Cash application for transactions with missing remittance detail involves additional manual steps before posting, which is most noticeable in exception-heavy environments. Standard payment flows align well with the platform’s core matching logic, supporting accurate and consistent processing.

What G2 users dislike about Billtrust:

“I don’t like that I can’t export an Excel spreadsheet from ‘search receivables’ under the ‘cash app’ tab. Also, the page will randomly time out on me while in the middle of work, causing me to do double work. Update the AI to support more technical issues and help with understanding things like what each queue is for, and how long it can take for the envelopes to process through.”

– Billtrust review, Lillian D.

2. Creditsafe: Best for credit risk assessment and business credit monitoring

Creditsafe is built to support everyday credit decisions by giving teams fast access to reliable company intelligence. It’s commonly used to assess who to extend credit to, on what terms, and with what level of risk, without adding friction to daily credit workflows.

Creditsafe directly supports daily credit assessment and limit-setting workflows. Teams can search companies quickly and access financial and corporate data in one place, which helps credit analysts set defensible limits without switching between tools. What I noticed in G2 reviews is that credit limit recommendations come up repeatedly as accurate and reliable, reflected in a feature rating of 88% on G2.

The platform surfaces risk signals clearly at the top of each report, giving credit teams a fast read on payment behavior and exposure before extending terms. That clarity supports quicker decisions on accounts that need closer scrutiny, which is reflected in an at-risk customers feature rating of 87% on G2.

The interface is straightforward, with fast access to company financials, credentials, and group structures without requiring training or a lengthy setup process. That accessibility extends to cost as well. G2 reviewers consistently describe Creditsafe as significantly affordable, which makes it practical for credit teams to run checks consistently across the full customer base rather than reserving pulls for only the highest-value accounts.

Creditsafe functions well as a reliable risk reference system rather than a purely predictive engine. What I noticed across G2 reviews is how often teams point to its credit scoring models and API access as practical advantages, allowing risk data to flow directly into ERPs or internal systems. This integration-first approach supports consistent credit checks without adding manual lookup steps, especially in finance-led credit operations.

When a company’s credit status, ownership, or financial position changes, Creditsafe surfaces that update without requiring manual re-checks. What struck me while going through the review data is how consistently teams describe responding to emerging risk early, rather than discovering issues only when a payment is already overdue. For credit teams managing large or frequently changing portfolios, that proactive signal reduces the gap between a risk event and a credit decision.

Teams can search by company name, address, or phone number, which helps locate the right entity quickly even when information is incomplete. The ability to generate a detailed PDF report on demand supports documentation and audit trails for credit decisions. Multiple G2 reviewers note this keeps credit evaluations fast and defensible without requiring additional tools or manual compilation.

A small number of G2 reviews mention that corporate hierarchy and ownership data can require closer review for complex group structures or entities that have recently changed ownership. Teams making credit decisions on multinational or frequently restructured entities will notice this more than those focused on straightforward assessments. For the majority of daily credit checks, the available structure data is sufficient to support fast, confident decisions. In most standard use cases, this balance of depth and usability helps teams move quickly.

International coverage varies by geography, with data depth tied to local reporting standards in each market. Teams running cross-border credit assessments in less-established markets will find the available detail more directional than comprehensive. For domestic credit assessment and monitoring across established markets, the data is consistently reliable and actionable.

Creditsafe continues to be a strong fit for credit and collections teams that need dependable company intelligence, clear risk indicators, and efficient daily workflows. Its strengths in credit limits, credit history, and at-risk customer visibility explain why it remains a commonly used decision-support tool in finance-driven credit environments.

What I like about Creditsafe:

- Core credit information is easy to access in one place, allowing quick review of credit limits, payment behavior, and company history without switching tools.

- It works well for day-to-day credit decisions. Clear visibility into at-risk customers and structured company data supports fast, defensible evaluations of new and existing accounts.

What G2 users like about Creditsafe:

“I appreciate how easy it is to find the information I need with Creditsafe. I can search by address and phone number, which is incredibly useful. The advanced search offers numerous fields that help me locate exactly the company I’m looking for. I also love that Creditsafe can generate a PDF report at my request, providing detailed information that I can conveniently save to my files. Additionally, the initial setup was straightforward. I received a link and signed up in just a few minutes, and we can have multiple logins for our company. This is particularly beneficial when several team members need to access creditworthiness information simultaneously. Overall, Creditsafe’s ease of use is a standout feature, as evidenced by my willingness to rate it a perfect 10 for user-friendliness.”

– Creditsafe review, Danielle M.

What I dislike about Creditsafe:

- Ownership hierarchies involving complex group structures or recently changed entities can require a closer review pass, though for the majority of everyday credit checks the available data supports fast, confident decisions.

- Data depth in some emerging or less-established markets is more directional than comprehensive, which is more noticeable for cross-border credit assessments, while established-market use cases align well with the platform’s data coverage.

What G2 users dislike about Creditsafe:

“I honestly can’t say I dislike anything about Creditsafe. The only thing to keep in mind is that you have to download each report before leaving it. If you click on the report again later, it will be counted as a new report and will add to your total usage for the year.”

– Creditsafe review, Stephanie H.

3. HighRadius Accounts Receivables: Best for enterprise AR automation

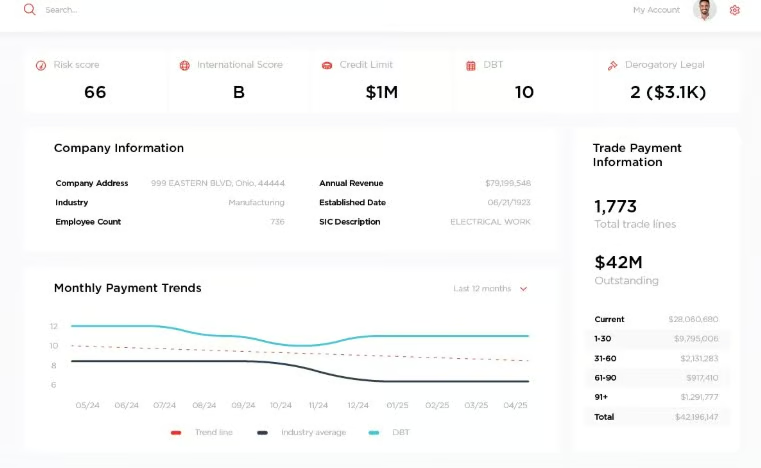

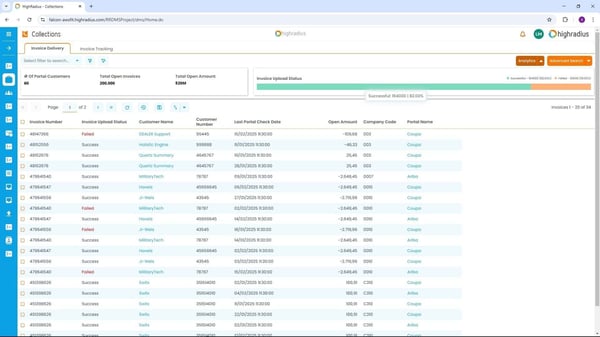

HighRadius Accounts Receivable is a platform designed for organizations managing large and complex receivables portfolios. It’s most often used where collections need to be standardized across teams and regions, reflecting environments that treat AR as a core operational function rather than a back-office task.

Based on G2 Data I evaluated, cash application stands out as a key differentiator for HighRadius, with teams moving away from spreadsheet-driven reconciliation toward automated matching and centralized worklists. Strong ratings for invoice and payment matching (79%) reinforce how well the platform supports consistent execution as volumes grow.

HighRadius performs well in Portfolio-level visibility. Customer accounts, deductions, and communication history are stored in one system, which improves coordination across AR, operations, and customer service teams. Retaining this context inside the platform reduces reliance on individual team members and supports better traceability over time, contributing to collections effectiveness (77%).

G2 reviews describe the interface as practical and process-oriented. Automation-driven worklists help standardize daily execution without forcing teams into constant manual tracking. The downstream effect is measurable. Collectors cover more accounts consistently, fewer invoices age without action, and throughput stays predictable even as portfolio size grows.

One thing I kept seeing across G2 reviews is measurable reductions in overdue balances described as a direct outcome of using the platform. Teams describe moving away from manual chasing and spreadsheet-driven tracking toward automated worklists that keep collections moving without constant oversight.

G2 reviews from teams operating at high invoice volumes describe notable improvements in how quickly outstanding balances are resolved, with some citing straight-through processing rates that would not have been achievable through manual methods alone. The collections team stops being a bottleneck and starts functioning as a decision layer, touching only the exceptions that genuinely need human judgment.

All customer correspondence, notes, and communication history are stored directly against each account within the platform. G2 reviews describe this as improving both traceability and continuity across AR teams, particularly in larger organizations where multiple people may touch the same account over time.”

From what I’ve seen across G2 review pattens, the platform automates the retrieval of supporting documents tied to deductions and chargebacks, pulling materials from customer portals without requiring analysts to chase them manually. What previously took hours of manual effort is handled systematically, freeing up analyst time for higher-value work, a capability teams have extended beyond its original deduction use case to credit issuance and other document-heavy workflows as well.

G2 reviewers point to trade-offs around credit workflow flexibility. Teams with frequently changing or highly custom policy requirements may find granular adjustments more configuration-driven than expected, while organizations operating stable, high-volume credit workflows align well with the platform’s consistent execution model. For teams with defined credit policies, this structured approach helps maintain consistency and reduces variability in decision-making at scale.

Deduction and email handling follow a defined workflow logic built for consistency and auditability across large AR operations. This structure is more noticeable for teams with non-standard communication setups or complex deduction structures, while organizations managing standardized collections processes align well with the platform’s approach to high-volume execution. In practice, this predictability supports cleaner audit trails and more reliable processing as transaction volumes grow

All in all, HighRadius Accounts Receivable is best suited for mid-market and enterprise credit and collections teams that need automation, portfolio visibility, and operational consistency at scale. These give mid-market and enterprise teams a stable operational foundation that scales with invoice volumes and portfolio complexity.

What I like about HighRadius Accounts Receivables:

- Automates cash application and AR workflows, reducing spreadsheet-driven effort at high payment volumes.

- Portfolio-level visibility across accounts and deductions keeps collections activity centralized and easier to manage at scale.

What G2 users like about HighRadius Accounts Receivables:

“I like HighRadius Accounts Receivables for its user-friendly design and how well it integrates with customers’ portfolios, providing shared visibility of the portfolio at all levels. I also appreciate the right level of details it offers to perform activities effectively, making portfolio review easier and improving navigation and traceability.”

– HighRadius Accounts Receivables review, Yendry R.

What I dislike about HighRadius Accounts Receivables:

- Teams with frequently changing or custom credit policy requirements may find granular adjustments more configuration-driven; once set up, the platform handles high-volume AR execution consistently and reliably.

- Deduction and email handling follow a defined workflow logic built for consistency across large AR operations. This is more noticeable for teams coming from ad hoc setups, while organizations managing standardized collections processes align well.

What G2 users dislike about HighRadius Accounts Receivables:

“The email inbox still has room for improvement. It would be helpful if email population based on prior communication worked more like Outlook. Currently, HighRadius only completes emails if the contact is in the account, but we have many contacts not stored to specific accounts. Having this feature would save a lot of time.”

– HighRadius Accounts Receivables review, Brittany M.

4. Quadient AR Automation by YayPay: Best for automated payment follow-ups

Quadient AR Automation (YayPay) supports receivables operations built for scale and consistency. It is a system built for day-to-day collections execution, where collectors actively manage account portfolios, track commitments, and monitor progress against monthly targets in one place.

G2 reviews frequently highlight automated dunning, portfolio-level visibility, and promise-to-pay tracking as core capabilities. Collectors managing large monthly balances describe relying on the platform to stay aligned with goals, reducing dependence on spreadsheets or ERP exports. This execution focus is reinforced by strong ratings for scalability (95%).

Common actions such as posting promises to pay, sending statements in bulk or individually, and tracking disputed invoices are described as straightforward across the G2 reviews I evaluated. Personalized customer messaging, rated at 92%, allows teams to maintain consistent outreach while tailoring communication without rigid templates. This balance, from what I’ve seen, supports sustained adoption in high-volume collections environments.

YayPay offers strong portfolio visibility. Collectors can view account status, open balances, disputes, and communication history in one place, which helps teams prioritize outreach and maintain continuity across follow-ups. According to G2 Data, customer profile scores 88%. This centralized context reduces reliance on individual collectors and improves handoffs when accounts change ownership.

YayPay is frequently used to reinforce accountability across collections teams. G2 users note that tracking commitments and follow-ups inside the system helps managers measure performance more consistently across portfolios.

Across G2 reviews I analyzed, dunning workflows vary meaningfully by customer segment, aging bucket, or account type, rather than sending identical messages across the entire portfolio. That flexibility allows collections teams to maintain a professional tone with key accounts while running automated, high-volume outreach on standard ones, without managing two separate systems.

Every customer interaction, invoice sends, payment discussions, dispute exchanges, is stored against the account within the platform. G2 reviews consistently note that having a complete, searchable email trail in one place removes the need to cross-reference inboxes or external email clients when reviewing account history. That continuity supports both daily collections execution and handovers when account ownership changes across the team.

G2 feedback points to one consistent trade-off around reporting: statement formats and dashboard views follow a structured layout that works well for standard collections needs but offers limited flexibility for teams that need custom output formats or cross-subsidiary reporting in a single view. This aligns most naturally with organizations focused on core collections execution, outreach, and portfolio management.

Some G2 reviewers note that workflow configuration and user management follow a defined setup model, which is more noticeable when building complex rules or managing large, frequently changing user bases. Teams with highly customized workflow requirements may find this more structured than expected, while organizations running standard AR operations align well with the platform’s approach to managing multi-account collections portfolios.

Quadient AR Automation is built for teams that value visibility, consistency, and scale in their receivables operations. Its strength in automation, late payment management, and portfolio-level execution makes it a strong fit for mid-market and growing organizations that need consistent collections cadence and team accountability month over month, not just during peak periods.

What I like about Quadient AR Automation by YayPay:

- It gives collections teams a clear daily workspace, keeping portfolios, promises-to-pay, disputes, and goals in one place.

- Automation improves payment follow-up without overriding collectors, reducing manual outreach while staying flexible at scale.

What G2 users like about Quadient AR Automation by YayPay:

“I rely on yaypay so much. It is the best app and helpful.It helps us to work on accounts at ease.”

– Quadient AR Automation by YayPay review, Simarpreet K.

What I dislike about Quadient AR Automation by YayPay:

- Reporting and dashboard views follow a structured layout that supports standard collections workflows well, though teams needing custom statement formats or cross-subsidiary reporting may find the configuration more limited.

- Building complex workflow rules or onboarding users mid-deployment follows a defined setup model that is more noticeable in large, multi-account environments.

What G2 users dislike about Quadient AR Automation by YayPay:

“My biggest gripe with Quadient AR is that the system does not send receipts automatically! My clients and my fellow AR staff think it is a HUGE miss in the system, and it should be part of every single package.”

– Quadient AR Automation by YayPay review, Finley P.

5. Tesorio: Best for treasury visibility and cash forecasting tied to collections signals

Tesorio is designed around execution-heavy AR work. The platform brings invoice visibility, customer communication, and collections prioritization into a single workflow, reflecting how finance and credit teams operate when collections signals drive forecasting decisions rather than static dashboards.

Tesorio removes manual effort from everyday collections tasks. While evaluating G2 reviews, I found teams consistently pointing to the ability to generate and download customer statements, review invoice status, and assess overdue balances without building aging reports or switching between systems. This reduction in manual prep helps teams focus more time on active follow-ups and resolution, consistent with a match invoices and payments score of 89% on G2.

Tesorio performs well in visibility into risk and late payment behavior. Based on my evaluation of G2 reviews, features like at-risk customers at 90% help teams quickly understand which accounts need attention and what is driving delinquency, supporting faster prioritization during daily collections cycles.

Centralized workflow management further supports consistent execution. Email outreach, invoice comments, customer notes, and resolution tracking all live within the same workspace, which helps maintain continuity across touchpoints. What became clear to me while reading G2 reviews is that having this context in one place reduces handoffs and prevents information gaps when accounts move between collectors or finance stakeholders.

Teams describe using urgency, balance size, and payment behavior to narrow daily workloads to accounts that require immediate action. That focus on actionable queues keeps collections effort concentrated where recovery is most likely, rather than spreading attention evenly across the full receivables ledger.

Teams describe moving away from manual spreadsheets toward a real-time view of expected cash inflows based on actual invoice and payment data. Finance leaders use the forecasting output directly in board reporting, reducing the gap between what collections teams know and what leadership sees. That connection between collections execution and cash forecasting is what separates Tesorio from platforms that treat the two as distinct workflows, reflected in an estimated vs actual receipts score of 85% on G2.

Invoice tags and notes improve daily collections coordination in ways G2 reviewers consistently flag. Tags allow teams to filter and prioritize accounts instantly, while notes against invoices or customer records stay visible across the finance organization. Customer profiles score a significant 91% on G2. In larger teams, that shared visibility reduces duplicated outreach and keeps everyone aligned on account status without separate updates or meetings.

Something worth keeping in mind is that automation follows a structured, rule-based approach rather than a self-directing or continuously adapting model. Users expecting the system to make independent decisions with minimal configuration will find the automation more guided than fully autonomous. G2 reviewers note that once workflows are set up, campaigns run reliably and execution stays consistent across collections cycles.

ERP synchronization runs on scheduled cycles rather than continuously. Finance teams depending on near-real-time invoice updates, particularly those running high-frequency billing or working across multiple time zones, will notice the sync gap most during active collections periods. G2 reviewers working within standard sync cadences describe the integration as stable and reliable in practice.

Tesorio stands out as a focused credit and collections platform built for teams that need reliable visibility into payment behavior and its impact on cash forecasting. It supports disciplined collections execution at scale. It fits best with mid-market and enterprise finance teams that treat collections as a signal-driven, operational function.

What I like about Tesorio:

- It centralizes invoices, balances, and customer communication, keeping collections work focused without jumping between systems.

- It’s also easy to prioritize accounts by urgency, dollar value, or risk. Late-payment visibility and at-risk customer insights help teams focus on the accounts that truly need follow-up as receivables volume grows.

What G2 users like about Tesorio:

“I love Tesorio because it saves me a lot of time by allowing me to download and customize customer statements easily. Unlike NetSuite, where customization wasn’t an option, Tesorio lets me skip creating an aging report manually. This efficiency reduces extra activities for me, making it very helpful. I also appreciate how Tesorio helps me check the status of invoices, see overdue amounts, and access pertinent comments and customer emails to verify their activity. The initial setup was quite easy too, which was a nice bonus.”

– Tesorio review, Aman K.

What I dislike about Tesorio:

- Rule-based automation suits teams that want reliable, predictable campaign execution, though those expecting the system to make independent decisions with minimal configuration will find the approach more guided than fully autonomous.

- ERP synchronization runs on scheduled cycles rather than continuously, which is most noticeable for teams running high-frequency billing or working across multiple time zones; teams operating within standard sync cadences align well with the platform’s integration model.

What G2 users dislike about Tesorio:

“The system can feel a bit basic and sometimes slow, especially when handling a large volume of invoices. The interface could be more intuitive, and a few improvements in speed and navigation would make it more efficient. It works, but there’s definitely room for enhancement to make the experience smoother.”

– Tesorio review, Verified user in computer software.

6. Upflow: Best for modern collections workflows with customer-friendly follow-up

Upflow is a credit and collections software that brings structure and predictability to collections workflows that no longer scale with manual follow-ups. It replaces spreadsheets and ad-hoc emails with a centralized system for tracking overdue invoices, standardizing outreach, and maintaining clear visibility into AR.

It supports consistent, timely follow-up at scale. Automated reminder workflows and clean invoice timelines help teams maintain cadence without relying on manual tracking. These capabilities are reflected in strong G2 ratings for features like late payments management and the customer portal (93%), which G2 users frequently describe as key productivity gains as collections volume increases.

The platform’s portal allows customers to view invoices, track payment status, and respond directly, reducing back-and-forth email traffic. G2 reviewers highlight how this improves professionalism in collections while preserving transparency, which is especially important for maintaining relationships as overdue balances grow.

While analyzing G2’s review data, I kept coming back to how consistently teams describe having a clear, up-to-date picture of AR, making it easier to prioritize outreach based on risk and urgency. This shared visibility supports better internal alignment between finance and sales teams by grounding follow-ups in consistent data rather than assumptions.

Upflow also supports learning-based optimization in follow-up workflows. Its adaptive learning feature, rated at 94% on G2, helps teams refine outreach timing and sequencing based on historical payment behavior. G2 users describe this as a way to improve response rates over time without adding manual analysis to daily collections work.

Ease of use contributes meaningfully to adoption, reflected in its ease of use G2 rating at 95%. One thing I couldn’t overlook in G2 review data is how often teams point to the intuitive interface and straightforward setup as reasons they onboard quickly without extensive training. For scaling finance teams that can’t absorb a long implementation runway, that matters practically. The platform starts returning value in weeks, without a dedicated rollout resource or extended handholding from the vendor.

Teams mention meaningful reductions in days sales outstanding after deploying the platform, with some noting improvements within the first few weeks of going live. The combination of automated follow-up cadences, workflow consistency, and clear prioritization means fewer invoices age without action, and payments come in on a more predictable schedule than manual processes typically allow.

A few G2 reviews note that payment reminder emails prioritize reliable delivery over visual customization, which is most noticeable for teams with strong branding requirements in customer-facing outreach. For teams focused on payment response rates, the format delivers consistently on schedule. G2 reviews describe the automated cadence as one of the clearest improvements to collections consistency after going live.

Reporting covers the metrics most collections teams need, but custom dashboard views and highly specific data slices fall outside what can be built directly within the platform. Finance teams that rely on granular, non-standard reporting will find some analyses require an export step rather than native configuration. G2 reviews working within the standard reporting scope find the available views as clear, actionable, and sufficient for daily tracking.

Upflow fits finance teams that want disciplined, customer-friendly collections without overengineering the process. For small and mid-market teams scaling AR volume, it provides a reliable operating layer that keeps collections focused, measurable, and repeatable as complexity grows.

What I like about Upflow:

- Automates invoice reminders and follow-ups, replacing manual emails and spreadsheets with a clear, centralized collections workflow.

- Provides strong visibility into past-due accounts through clean timelines, prioritization, and a customer payment portal.

What G2 users like about Upflow:

“I appreciate Upflow’s fantastic onboarding process and training, which made me feel very comfortable launching after preparing. Their payment portal is a great feature, offering a solution we didn’t have before. The automated reminders are incredibly useful, making Upflow a major convenience in comparison to what we used previously.”

– Upflow review, Zack M.

What I dislike about Upflow:

- Payment reminder emails are optimized for consistent automated delivery rather than visual branding, something that matters more to teams with heavily designed invoice communications than to those focused primarily on payment response rates. This helps ensure reminders go out reliably.

- Custom dashboard views and highly specific data slices fall outside what can be built natively within the platform; for teams with standard AR tracking needs, the built-in reporting is clear, actionable, and sufficient for daily use. This simplicity makes it easier for teams to monitor performance.

What G2 users dislike about Upflow:

“The main downside is that some reporting and filtering can feel a bit rigid when I want to slice data in very specific ways. There are moments where I’d like more flexibility in customizing views or building my own AR dashboards. That said, these are refinements, I still find the platform very valuable overall and rely on it daily.”

– Upflow review, Pamela E.

Running collections cadences but still forecasting in spreadsheets? The best budgeting and forecasting software covers how finance teams build rolling plans that reflect what AR is actually telling them.

7. Gaviti: Best for AR automation with configurable collections policies

Gaviti focuses on the core mechanics of accounts receivable and collections, helping teams track overdue invoices, manage follow-ups, and keep internal teams and customers aligned. It functions as an operational hub for AR teams that need structure, visibility, and consistency in their collections workflow, replacing spreadsheets and ad-hoc communication with repeatable processes.

Gaviti’s strongest capabilities map directly to disciplined collections execution. Scalability, rated at 83%, reflects how the platform supports higher invoice volumes and multi-account management without breaking visibility, helping teams focus effort on accounts that need immediate attention.

What I noticed in G2 reviews is that the platform simplifies communication and accountability across teams in a way that sticks. Automated reminders, shared task visibility, and centralized correspondence help finance and operations stay aligned without losing track of any touchpoint, and having every note, reminder, and correspondence accessible in one place keeps daily collections moving and reduces manual coordination.

G2 reviews mention the user-friendly interface and ease of onboarding, reflecting in ease of setup score of 87% on G2 . Several users note that new team members can be trained quickly and begin contributing to collections work without steep learning curves. That usability supports productivity from the early days of deployment, a common signal in G2 feedback.

Gaviti also earns praise for operational efficiency enhancements like bulk editing and dispute assignment. The feedback highlights features such as the ability to pause invoices within workflows, assign disputes to the right colleagues, and perform bulk edits, all of which reduce repetitive manual tasks and free up time for higher-value work.

Based on my evaluation, I found that reporting and cash flow visibility are handled in a practical, accessible way that finance teams at this scale genuinely rely on. Dashboard reports and invoice due-date filters are flagged as especially useful for monitoring receivables and supporting short-term forecasting, with promise-to-pay tracking and easy Excel exports allowing teams to adapt reporting for leadership without rebuilding datasets.

G2 reviews describe separate collection paths for different customer types as central to daily AR work. Gentle reminders run for lower-risk accounts while escalating workflows run simultaneously for higher-exposure ones. That segmentation keeps outreach proportionate to risk, reducing friction with reliable payers while maintaining follow-up where it matters most, supported by a late payments score of 86% on G2.

Some G2 reviewers note that customer statements focus on active collections and due items rather than full account summaries. This is more noticeable for teams that regularly share comprehensive views including future invoices and credits, while collections-focused workflows align well with the emphasis on current and overdue items. For teams prioritizing collections efficiency, this focus helps keep communication clear and action-oriented without unnecessary detail.

Performance and responsiveness can vary when multiple users are active simultaneously. This is more noticeable for teams running high-concurrency operations during peak periods, while smaller or staggered user environments align well with the platform’s standard collections workflows. In typical day-to-day usage, teams report stable performance that supports consistent execution across standard collections tasks.

All in all, Gaviti is well-suited for accounts receivable and finance teams that want tighter receivables control, clearer prioritization, and consistent follow-up workflows. It works best for organizations that value discipline and visibility in their credit and collections process.

What I like about Gaviti:

- Gaviti centralizes overdue tracking, at-risk accounts, and follow-ups, helping teams stay focused on collections without manual chasing.

- G2 users also value its cash flow visibility through dashboards, due-date filters, and promise-to-pay tracking.

What G2 users like about Gaviti:

“One of the newer things I appreciate about Gaviti is how effectively it keeps our team focused on daily tasks while seamlessly keeping customers updated on their invoices, including the ability to automatically send large attachments. The customer support team is very responsive and helped us smoothly integrate Gaviti’s features into our daily routine.”

– Gaviti review, Adeajai P.

What I dislike about Gaviti:

- Statement output covers active collections and due items, so teams that routinely share full account summaries will need additional steps outside the platform. For collections-focused workflows, the scope keeps daily execution focused and manageable.

- Page performance can slow under heavy concurrent usage during peak periods, though outside those windows navigation is straightforward and the platform handles standard collections execution reliably.

What G2 users dislike about Gaviti:

“The cash application section is less user-friendly compared to the collections and disputes sections. It also lacks the range of options needed to handle the various situations that can arise during cash application. Integration for the cash app was not ease and fast as expected.”

– Gaviti review, Tijana P.

8. Global Database Risk Intelligence: Best for global company risk intelligence

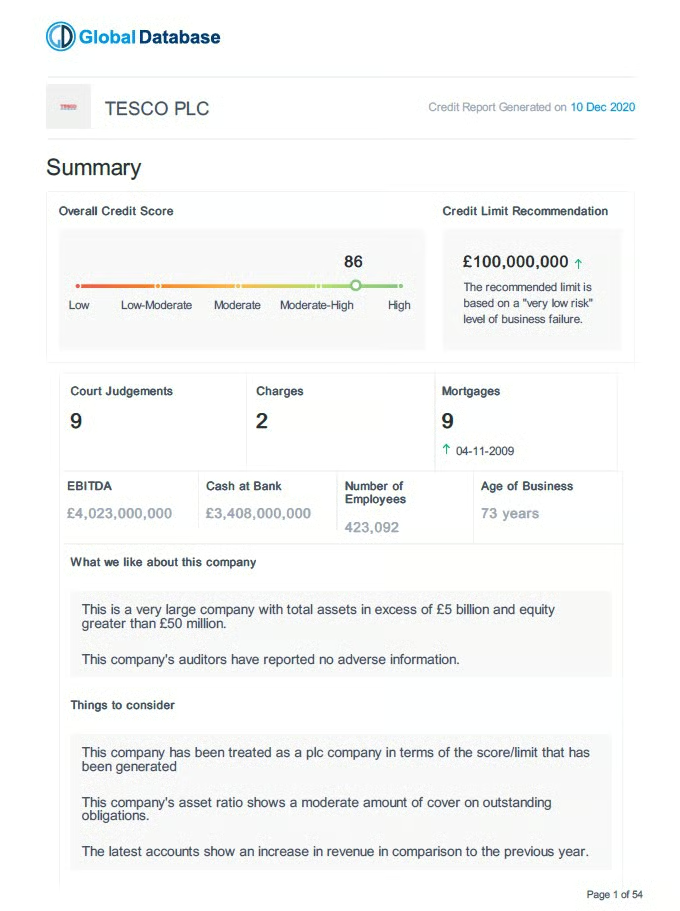

Global Database Risk Intelligence (GDRI) is used by teams that need to assess counterparty risk before extending credit, setting limits, or offering insurance coverage, particularly when working with international buyers, partners, or borrowers.

It is designed to support credit decisions where local bureau data alone is insufficient, and where ownership structure, historical behavior, and cross-border visibility matter.

What stood out to me first across G2 reviews is how GDRI consolidates credit intelligence that’s typically fragmented. Teams can access historical credit ratings, payment behavior, court judgments, ownership structures, and group relationships in one place. This unified view helps credit teams move from snapshot assessments to risk evaluation grounded in longer-term patterns, supported by a credit history score of 99% on G2.

Proactive risk monitoring is another area where GDRI performs well. Multi-step planning, personalized customer messaging, and credit limit suspension all receive 100% ratings on G2. The alerts around credit status changes, ownership updates, and corporate restructuring as especially valuable for staying ahead of emerging risk instead of reacting after issues surface.

G2 user feedback also highlights the measurable impact of this depth of insight. What I picked up while studying G2’s review data is that teams report faster underwriting cycles and fewer manual re-evaluations once GDRI replaces generic bureau data. Reviewers consistently say this shift is one of the clearest signs that better data leads to faster, more confident credit decisions.

Credit and compliance data flows directly into CRM platforms like Salesforce and HubSpot rather than requiring manual lookup and entry. Company profiles, ownership details, and risk scores stay current without additional effort from the team. For organizations running credit assessments alongside sales or procurement activity, that automatic enrichment keeps company profiles, ownership details, and risk scores current without anyone on the team having to maintain them.

G2 reviews in compliance-heavy industries describe GDRI covering sanctions, PEP screening, adverse media, and ultimate beneficial ownership data alongside credit scoring. Teams in export credit insurance, logistics, and financial services use this to vet counterparties against compliance and credit requirements simultaneously, removing the need for parallel checks across separate tools.

Risk intelligence is only useful if the people acting on it can navigate the platform without friction. While going through hundreds of G2 reviews, I noticed that teams across compliance, operations, and finance consistently describe the dashboard as clean and accessible to non-financial users, with ownership summaries, risk scores, and payment histories surfacing clearly at a glance. For organizations where credit decisions involve stakeholders beyond the core credit team, that readability reduces the interpretation layer between data and action.

Alerting is intentionally comprehensive, and some G2 reviewers note that daily summaries can include updates that are not immediately actionable for every role. Teams managing large portfolios across multiple responsibility levels will notice the volume of alerts more than smaller or single-function teams. The underlying monitoring capability itself is consistently described by G2 reviewers as a core strength of the platform.

Data availability varies by geography, with financial disclosures in certain emerging markets or for newly formed companies being more limited than in mature economies. Teams running credit assessments heavily weighted toward these markets will find the available data more directional than comprehensive. G2 users mention GDRI delivers consistently reliable and actionable financial insight for established markets and standard credit workflows.

Global Database Risk Intelligence works best for organizations that care more about understanding who they are extending credit to, and the structure behind that risk. For global credit, insurance, and risk teams, GDRI strengthens decision confidence where surface-level scores fall short.

What I like about Global Database Risk Intelligence:

- GDRI centralizes global credit data, ownership structures, payment behavior, legal signals, and historical trends, so teams don’t need to rely on fragmented local bureau reports.

- G2 Reviewers consistently point to proactive alerts and historical credit visibility as major strengths, helping teams react quickly to changes in counterparty risk.

What G2 users like about Global Database Risk Intelligence:

“The feature I appreciate most is the way Global database risk intelligence surfaces not just the current credit rating but shows historical trend data, payment behavior, court judgements and group relationships. For our SME lending business, that context is priceless.”

– Global Database Risk Intelligence review, Jim Y.

What I dislike about Global Database Risk Intelligence:

- Daily alert summaries are intentionally broad in their counterparty monitoring coverage, which means teams managing large portfolios across multiple responsibility levels may want to refine their alert setup to filter lower-priority updates; the underlying monitoring depth itself is consistently well-regarded.

- Financial data availability in certain emerging markets reflects local disclosure norms rather than platform limitations, so teams with significant exposure in those regions will find specific cases more directional than comprehensive while coverage across established markets remains strong.

What G2 users dislike about Global Database Risk Intelligence:

“The only aspect that I found slightly cumbersome is the initial setup of our customer risk score parameters to better align with our internal policy. It required several meetings with the support team to fine tune the thresholds, but once configured the process has become smooth. ”

– Global Database Risk Intelligence review, Debarshi M.

9. Versapay: Best for collaborative AR and buyer-facing payment experiences

VersaPay helps finance teams manage receivables, payments, and customer follow-ups through a more structured, digital-first workflow. It is a system optimized for operational consistency, one that focuses on accelerating cash collection while reducing friction for both AR teams and customers.

I noticed a pattern in G2’s reviews around payment posting, teams consistently describe it as one of the more reliable parts of the Versapay experience. Teams highlight how smoothly payments are applied once received, with the AR invoice closing in the ERP in real time after a customer pays. That accuracy reduces reconciliation effort and keeps AR balances current without manual intervention, reflected in a cash application feature rating of 92% on G2.

Teams describe being able to send invoices, issue statements, and track overdue balances without switching between systems, with customers able to access their documents directly through the portal. Financial documents and late payments are both rated at 89% on G2, reflecting how consistently the platform supports document delivery and overdue follow-up in day-to-day AR work.

Support responsiveness plays a meaningful role in how teams perceive the platform, and it is something I validated from G2 reviews rather than assumed. Reviewers highlight timely, hands-on assistance from the VersaPay team, including support during urgent payment-processing incidents that affected large customer groups, the kind of responsiveness that matters for finance teams relying on the system for uninterrupted daily collections execution.

Feedback highlights a specific capability that matters in daily collections: the ability to see whether a customer has opened and viewed an invoice. That visibility removes ambiguity from follow-up conversations, since AR teams can confirm delivery rather than relying on customer claims that invoices were not received. This is directly improving collections accountability and reducing delays caused by disputed delivery.

Users who run Versapay alongside NetSuite and other ERP systems consistently note how cleanly the platform connects with their existing setup. Payments made through the portal close the corresponding invoice in the ERP in real time, which eliminates manual reconciliation steps and keeps AR balances accurate throughout the day.

That tight integration reduces the back-and-forth between systems and keeps collections data and financial records aligned without additional effort, supported by an incomplete payments score of 81% on G2.

Customers can log in at any time to view open invoices, check account balances, make ACH or credit card payments, and access statements without contacting the AR team. G2 reviewers note this self-service access reduces inbound payment-related calls and emails, freeing collections staff for active follow-up work. Automated dunning runs alongside the portal to handle consistent outreach on standard accounts, so the two capabilities reinforce each other without requiring parallel management.

While overall feedback is strong, G2 reviewers note that reporting and analytics are built around standard AR visibility rather than configurable outputs. Teams that need historical data exports at scale or custom reporting slices will find some analyses require exporting data outside the platform to complete. For routine collections monitoring and receivables tracking, the built-in views are clear and sufficient.

Post-launch support response times come up in G2 reviews as an area where the experience can vary. Teams that encounter issues after go-live describe waiting longer than expected for resolution, which creates friction for finance teams running time-sensitive collections workflows. The implementation and onboarding experience is consistently described as smooth, and the platform itself runs reliably once configured.

VersaPay aligns well with mid-market credit and collections teams that want to collect cash faster, maintain clean receivables, and offer customers a clear, self-service payment experience.

What I like about Versapay:

- VersaPay streamlines collections with self-service payments, automated dunning, and clear receivables visibility, helping teams collect cash faster with less manual follow-up.

- Its ease of use stands out, with G2 reviewers highlighting accurate financial data and reliable cash application, reflected in strong ratings for Cash Application (92%) and Financial Documents (89%).

What G2 users like about Versapay:

“They are very responsive and help out and continue to work until they resolve any issues or concerns.”

– Versapay review, Patricia L.

What I dislike about Versapay:

- Reporting is built around standard AR visibility rather than configurable outputs, which creates friction for teams that need historical data exports at scale or non-standard reporting slices; for everyday collections monitoring the built-in views are sufficient and easy to act on.

- Post-launch support response times can vary, something that affects teams more during active issue resolution periods than during steady-state operations; the platform itself runs reliably once set up and the onboarding experience is consistently well-regarded.

What G2 users dislike about Versapay:

“A couple of times I have observed that we are unable to remove a bank account on behalf of our customers which becomes a bit stressful for them. They have to disable the autopay, select another account and then delete the primary account. This process can be made more efficient.”

– Versapay review, Deep P.

10. Resolve: Best for AI-assisted collections and dispute resolution workflows

Resolve supports teams that want to offer payment terms and manage collections without adding ongoing manual work. It handles credit onboarding, invoicing, and automated follow-ups so finance teams can extend Net-30 terms and keep cash moving without dedicating constant time to chasing payments.

Automated reminders and weekly customer statements remove the manual follow-up burden from small finance teams, with collections activity running consistently in the background without constant oversight. Invoice records, customer data, and payment history stay organized and easy to reference within the platform. This means the team spends less time locating information and more time on the accounts that actually need attention.

Cash inflows become more predictable when follow-ups run on a consistent schedule rather than depending on someone remembering to chase. For SMBs, that shift in how collections works carries more operational weight than sophisticated tactics or heavy configuration ever could.

Financial documents and customer profiles are rated at 97% on G2, a signal that the platform handles the foundational mechanics of invoicing and payment recordkeeping with consistent accuracy. For teams extending terms to new customers, that reliability matters most when credit decisions need to be made quickly and the underlying data has to be trusted.

Customers can apply for terms online, and businesses are typically notified within about 24 hours of whether credit can be extended. G2 reviewers often mention that this makes it feasible to offer Net-30 to customers who would normally decline, and with an at-risk customers score of 95% on G2, the platform’s visibility into exposure helps businesses stay confident about who they are extending those terms to.

Support quality also plays a meaningful role in user satisfaction. While analyzing G2’s reviews, I kept landing on the same insight around support — several reviewers highlight having a consistent point of contact who understands their account history and setup. For small teams, that continuity reduces back-and-forth and makes ongoing operations steadier.

Resolve allows businesses to offer Net-30 terms without taking on the credit risk themselves. When a customer is approved, the business gets paid while Resolve manages the exposure, removing the barrier to offering terms competitively. G2 reviews from tight-margin industries describe this as opening up new business with customers who previously could not pay upfront, without building an internal credit function. That model is backed by a credit limits adjustment score of 92% on G2.

Across G2 reviews, I see one trade-off come up around credit configuration depth. Businesses with non-standard credit policies or tiered limit structures will find the available options more limited than a dedicated enterprise credit platform. G2 reviewers running standard Net-30 setups describe the credit workflow as simple, fast, and easy to manage without dedicated overhead.

Refund handling can require additional coordination, particularly when refunds need to be processed back to the original payment method. Teams that handle frequent adjustments or post-payment corrections may encounter a few extra steps in those specific scenarios, while day-to-day collections and invoicing remain unaffected, and G2 reviewers describe the core payment management experience as reliable and consistent.

Resolve Pay fits best for businesses that want to offer payment terms, automate collections follow-ups, and reduce manual effort without building a full credit and collections operation. Execution, consistency, and ease of use define Resolve. It suits businesses that want credit and collections to run with minimal overhead, freeing the team to focus on growth rather than chasing payments.

What I like about Resolve:

- It simplifies extending payment terms by combining credit onboarding, invoicing, and automated reminders into one workflow, which reduces manual follow-ups and keeps collections predictable.

- It is easy for customers to apply for Net-30 terms, and how quickly credit decisions are communicated, making it easier to offer terms without slowing down sales or finance operations.

What G2 users like about Resolve:

“We have been partnering with Resolve since 2018 and they have been integral to our growth. Their team is always willing to assist us and over the years they have made onboarding our clients very easy. The credit application is easy for both our clients and us making terms implementation simplified. Our clients can easily apply for credit terms online and we’re notified by ResolvePay within 24 hours typically on whether or not we can extend terms to our clients.”

-Resolve review, Tobi D.

What I dislike about Resolve:

- Platform updates occasionally shift where features and settings are located within the interface, creating a brief reorientation period after releases; invoice editing also has some scope limits around same-day changes, though the core team is responsive to feedback.

- QuickBooks synchronization requires some manual coordination in specific transaction scenarios, which affects teams running Resolve alongside QB more than those on other integrations; day-to-day invoicing and collections run smoothly within standard flows.

What G2 users dislike about Resolve:

“Late fees can be troublesome for customers. Some transactions require some extra work to communicate correctly with QB and some information doesn’t flow back and forth between the two platforms.”

– Resolve review, Mitchell M.

Comparison of the best credit and collections software

|

Software |

G2 rating |

Free plan |

Ideal for |

|

Billtrust |

4.4/5 |

No |

Invoice-to-cash automation across complex B2B billing environments with fragmented customer bases |

|

Creditsafe |

4.4/5 |

Free trial available |

Credit risk assessment, business credit monitoring, and upfront credit decisioning |

|

HighRadius Accounts Receivables |

4.3/5 |

No |

Enterprise-grade AR automation, AI-driven prioritization, and forecasting at high invoice volumes |

|

Quadient AR Automation by YayPay |

4.4/5 |

No |

Intelligent collections workflows, automated outreach, and promise tracking |

|

Tesorio |

4.7/5 |

No |

Treasury visibility and cash forecasting tied directly to AR and collections signals |

|

Upflow |

4.8/5 |

Yes. Free plan available |

Modern, customer-friendly collections workflows for scaling finance teams |

|

Gaviti |

4.5/5 |

No |

AR automation with configurable collections policies and customer segmentation |

|

Global Database Risk Intelligence |

4.8/5 |

Free trial available |

International credit risk analysis and global company intelligence |

|

Versapay |

4.1/5 |

No |

Collaborative AR workflows and buyer-facing invoice and dispute management |

|

Resolve |

5.0/5 |

No |

AI-assisted collections and dispute resolution with human-in-the-loop control |

*These credit and collections software are top-rated in their category, based on G2’s Winter Grid® Report. All offer custom pricing tiers and demos on request.

Best credit and collections software: Frequently asked questions (FAQs)

Got more questions? G2 has the answers!

Q1. What are the top tools for automating collections workflows?

Based on G2 review patterns, HighRadius Accounts Receivable, Quadient AR Automation (YayPay), Upflow, and Gaviti stand out for collections automation. These platforms consistently reduce manual follow-ups through automated reminders, task generation, promise-to-pay tracking, and prioritized worklists, while still keeping collectors in control of exceptions.

Q2. Which are the top platforms for real-time collections reporting?

Tesorio, Billtrust, and Upflow are most frequently cited for strong collections visibility. Tesorio connects overdue signals directly to cash forecasting. Billtrust surfaces real-time invoice delivery and payment status, useful in high-volume B2B environments. Upflow gives finance and sales teams a shared, up-to-date AR picture without manual reporting overhead.

Q3. What are the best platforms for integrating credit management with ERP?

Billtrust, HighRadius, Quadient AR Automation, and Tesorio are commonly used alongside ERPs such as SAP and NetSuite. These tools are designed to synchronize invoice data, payments, and collections activity with accounting systems, reducing manual reconciliation and preserving a single system of record.

Q4.What are the best tools for tracking overdue payments?

Upflow, Gaviti, Quadient AR Automation, and Tesorio consistently perform well for overdue tracking. Upflow and Gaviti focus on invoice timelines, automated reminders, and segmented collection paths. Quadient AR Automation centralizes promise-to-pay tracking and aging in one collector workspace. Tesorio lets teams filter by urgency, balance, and payment behavior to prioritize accounts that need immediate action.

Q5. Which is the best credit and collections software for finance teams?

There’s no single best credit and collections software for every finance team. Billtrust works well for complex B2B billing and high payment volumes. HighRadius fits larger organizations that need scaled automation and tighter operational control, while Upflow and Gaviti are better suited for growing teams that want structured collections without heavy complexity. The right choice depends on your invoice volume, workflow maturity, and cash visibility needs.

Q6. What are the top-rated credit and collections platforms for large enterprises?

HighRadius and Billtrust are the most commonly selected by enterprise teams. HighRadius handles large, complex portfolios with AI-driven worklists, automated cash application, and deduction management at scale. Billtrust suits high-volume B2B environments with complex remittance, offering automated payment matching, invoice distribution, and customer self-service portals.

Q7. Which platform is best for compliance with debt collection laws?

Billtrust, HighRadius, and Versapay are frequently used in regulated environments. Billtrust maintains structured audit trails across invoice delivery and payment application. HighRadius applies defined workflow logic to deductions and communications, keeping AR traceable across large teams.

Q8. What is the best software for managing credit approvals?

Creditsafe and Global Database Risk Intelligence are most commonly referenced for credit assessment and approvals. Creditsafe gives analysts fast access to credit limit recommendations, payment behavior, and risk scores, with API integration that feeds decisions directly into ERPs.

Q9. Which software offers AI-powered credit risk analysis?

HighRadius Accounts Receivable and Resolve include AI-assisted capabilities. HighRadius applies AI to prioritization and forecasting in large AR portfolios, while Resolve uses automation and decision logic to support SMB credit onboarding and payment terms without heavy manual oversight.

Q10. Which credit and collections software offers the lowest fees?

Pricing varies by use case and volume, and most tools offer custom pricing. Upflow is the only platform in this list with a publicly available free plan, making it accessible for smaller or scaling teams. Other platforms prioritize value at scale rather than the lowest upfront cost.

From overdue to under control

Credit and collections software isn’t a temporary fix. Over time, it becomes part of how teams manage risk, prioritize follow-ups, and track cash flow day to day. The difference shows up in execution: what gets attention, what gets delayed, and how much manual effort is needed to keep collections moving.

From what I’ve seen across G2 reviews, the strongest platforms reduce that friction. They make ownership clearer, cut down on repetitive work, and help teams stay consistent as invoice volume grows.

Over time, the impact compounds. Teams move from reacting to overdue accounts and disputes to managing collections more proactively. When the fit is off, the opposite happens, manual work increases, accountability gets blurred, and forecast confidence weakens.

That’s why this decision is less about feature depth and more about workflow fit. Different teams need different levels of visibility, automation, and control. The right platform supports how your finance team already operates while helping it scale without adding complexity.

Want to strengthen receivables end-to-end? Explore accounts receivable automation tools on G2 to improve cash predictability and reduce friction early.

💸 Earn Instantly With This Task

No fees, no waiting — your earnings could be 1 click away.

Start Earning